Coliving Finances

1. The Rise of Coliving Investments - Coliving Finances

If you came to this article directly, consider going through the series of articles it is a part of. Please find the link to the other articles in the...

June 11, 2025

From seed rounds to institutional capital — equity structures, investor landscape, pitch deck essentials, unit economics, and the financial metrics coliving investors demand in a $7.8B+ market.

Interactive calculators and tools to put these insights into action.

Generate an investor pitch outline with financial projections.

Try it free →Estimate potential returns and payback periods for coliving.

Try it free →Build a comprehensive operating budget for your property.

Try it free →Estimate coliving demand in your target market.

Try it free →Global Coliving Market (2024)

Industry Average Occupancy

Income Premium vs Traditional

Institutional Capital Committed (EU)

Coliving is simultaneously a real estate play and an operating company. This duality creates unique fundraising challenges — and opportunities. Unlike pure real estate (where capital follows cap rates) or pure tech (where capital follows growth metrics), coliving investors evaluate both property-level economics and operational scalability.

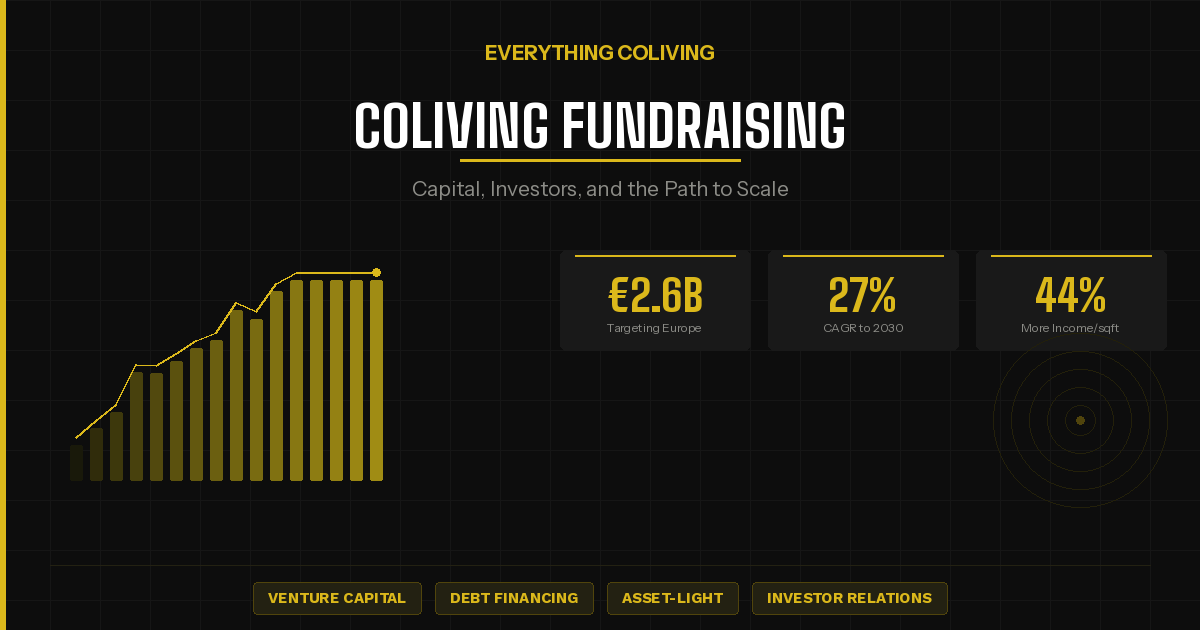

The global coliving market reached $7.82 billion in 2024, growing at 11–13.5% CAGR. Institutional capital is flowing in: 38% of European investors with €1 trillion+ AUM are already invested in coliving, with 51% planning to invest within three years. But the landscape is also marked by cautionary tales — Common Living’s $110M+ bankruptcy in 2024 reshaped how investors evaluate the sector.

This guide draws on the Art of Coliving real estate and growth pillars, industry data from our Global Coliving Report, and analysis of $5B+ in coliving deals to give you the most comprehensive fundraising framework available.

Your fundraising strategy depends on your business model, space design, and community experience — these pillar pages complement this guide. For a complete overview of launching a coliving business, see our Complete Coliving Guide.

Need help with your coliving fundraising strategy? Our advisory team has helped raise capital and structure deals for 60+ coliving projects across 14+ countries.

Each funding stage has different investors, instruments, and milestones. Understand where you are and what it takes to reach the next level.

Capital Sources

Personal savings, friends & family, angel investors, small grants

Instruments

SAFEs, convertible notes, or personal capital

Milestones Required

First property secured (lease or purchase), initial resident traction, proof of concept with positive unit economics.

Capital Sources

Angel investors, impact funds, seed-stage VCs, real estate family offices

Instruments

SAFEs (64% of seed deals), priced equity (27%), convertible notes (10%)

Milestones Required

1–3 stabilized properties at 90%+ occupancy, proven unit economics, clear community engagement metrics, repeatable acquisition playbook.

Capital Sources

PropTech VCs, real estate PE firms, institutional impact investors, strategic hospitality partners

Instruments

Priced equity (Series A Preferred), venture debt, revenue-based financing

Milestones Required

5–15 properties, 500+ beds under management, demonstrable path to 15%+ EBITDA margins, scalable operating platform.

Capital Sources

Institutional PE, sovereign wealth, pension funds, dedicated coliving funds, REIT structures

Instruments

Priced equity, mezzanine debt, project finance, fund structures

Milestones Required

1,000+ beds, multi-city presence, strong NOI track record, institutional-grade reporting, experienced management team.

Our advisory team has helped structure deals and raise capital for 60+ coliving projects globally.

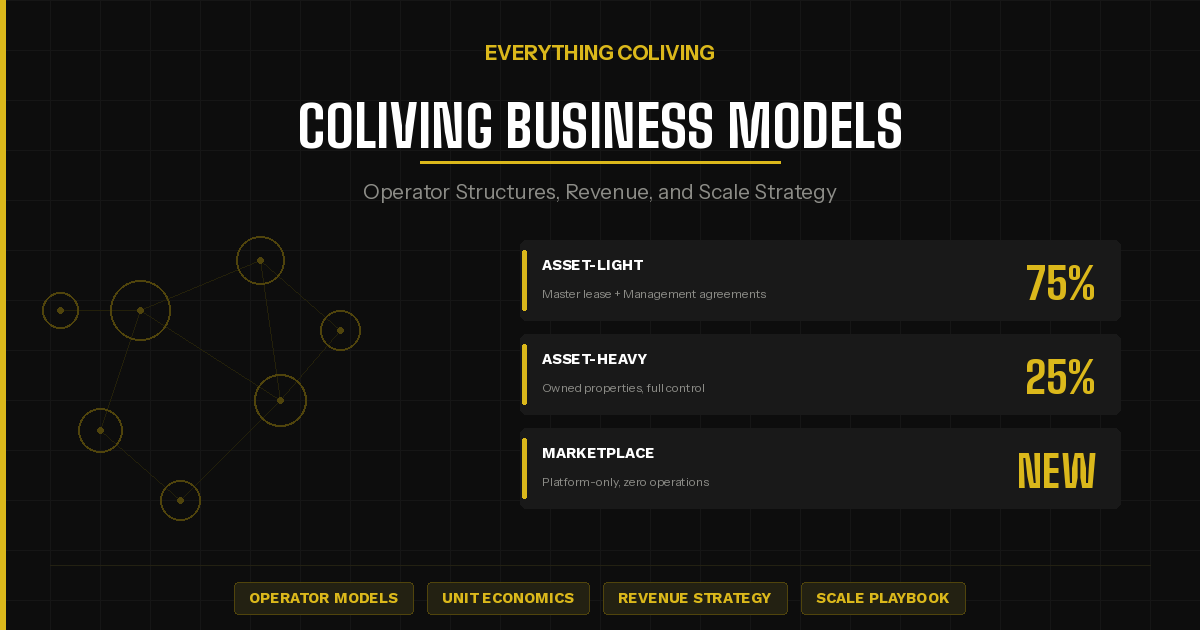

Your investment model determines your capital needs, risk profile, and investor appeal. Post-2024, the market has shifted toward ownership and management agreements.

Operator leases entire property from landlord and subleases individual rooms to residents. Fixed or performance-based rent to the owner.

Capital Required

Low

Risk Profile

High

Operator Control

Medium

Typical Margin

15–30% gross margin if well-managed

Investor Appeal: Lower — occupancy risk sits with operator. Post-2024 caution after Common bankruptcy.

Best for: Early-stage operators validating the model; markets with available multi-unit buildings.

Operator or investor acquires property outright, converts or builds for coliving, and operates in-house or via management company.

Capital Required

Very High

Risk Profile

Moderate

Operator Control

Full

Typical Margin

40–60% gross margin with scale; 10–30% NOI premium over traditional residential

Investor Appeal: Highest — asset appreciation + operating income. Preferred by institutional investors.

Best for: Institutional capital, long-term hold strategies, markets with strong capital growth.

Operator manages property on behalf of owner for a fixed fee or revenue share (typically 10–20% of collected rents).

Capital Required

Minimal

Risk Profile

Low

Operator Control

Low–Medium

Typical Margin

Management fee: 10–20% of revenue; performance bonuses possible

Investor Appeal: Growing — asset-light, scalable. Preferred post-2024 by operators seeking sustainable growth.

Best for: Experienced operators scaling rapidly; real estate investors seeking coliving management.

Operator co-invests with real estate partner. Shared ownership with operational responsibilities split by expertise.

Capital Required

Medium

Risk Profile

Moderate

Operator Control

Shared

Typical Margin

Varies — equity split typically 20–40% operator, 60–80% capital partner

Investor Appeal: Strong — aligned incentives between operator and capital partner. Reduces operator capital needs.

Best for: Operators with operational track record partnering with real estate investors.

The Art of Coliving identifies four prime real estate opportunities for coliving operators — each with different capital requirements and return profiles.

Hotels with 20–25% occupancy can be converted to coliving at lower cost than new builds. Post-COVID, the hospitality sector created a wave of available properties.

Advantage: Existing bedrooms, common areas, and hospitality infrastructure reduce conversion costs.

Remote work has created a surplus of vacant office space. Zoning changes are increasingly allowing commercial-to-residential conversion.

Advantage: Large floorplates ideal for cluster-based coliving design. 25–35% lower conversion costs than traditional apartment development.

Industrial buildings in gentrifying neighborhoods offer large, affordable spaces with character and community appeal.

Advantage: High ceilings, open plans, and cultural character create unique coliving brands. Opportunity zone incentives may apply.

Designed from scratch for coliving — optimal cluster sizing, shared-to-private ratios, and community infrastructure.

Advantage: Highest operational efficiency and NOI. Attracts institutional capital. UK planning applications up 87% YoY in 2024.

Two proven strategies from the Art of Coliving: (1) Expensive cities with high demand — metropolitan areas where flexible, affordable housing stands out; and (2) Just behind the wave of gentrification — areas that will gentrify within 5–10 years, where coliving can be a catalyst for neighborhood development and brand building. For your space design, consider how property type affects cluster sizing and community layout.

Know these metrics cold. Every serious investor conversation will center on these numbers — they separate operators who understand their business from those who don’t.

| Metric | What It Measures | Benchmark | Priority |

|---|---|---|---|

| RevPAB Revenue Per Available Bed | Total revenue divided by total available beds (occupied or not). The primary coliving performance metric — equivalent to RevPAR in hotels. | Varies by market; has outperformed hotel RevPAR globally | High |

| Occupancy Rate Bed/Room Occupancy | Percentage of available beds occupied over a given period. The most fundamental coliving health indicator. | Target: 90–100%; Industry average: 93–94% | Critical |

| NOI Net Operating Income | Total revenue minus operating expenses (before debt service and taxes). Measures property-level profitability. | Coliving densification increases NOI 10–30% vs traditional apartments | Critical |

| Cap Rate Capitalization Rate | NOI divided by property purchase price. Indicates annual return on an all-cash basis. | Coliving: 4–7% (Europe); Sydney 4% vs 2.6% traditional; Hong Kong 3.4% vs 2.2% | High |

| IRR Internal Rate of Return | Total annualized return accounting for all cash flows over the hold period. More comprehensive than cap rate for development and value-add deals. | Target: 15–25% for value-add; 8–12% for stabilized core | High |

| CAC Customer Acquisition Cost | Total marketing and leasing spend divided by number of new residents acquired. Investors track CAC trends over time. | $300–500 per bed; declining CAC signals operational maturity | Medium |

| LTV / LTV:CAC Lifetime Value & LTV-to-CAC Ratio | Revenue generated per resident over their entire stay. LTV:CAC ratio of 3:1+ considered healthy. With 9-month average stays, LTV = ~$9,000+ per resident. | LTV:CAC > 3:1; Average stay: 9 months | Medium |

| DSCR Debt Service Coverage Ratio | NOI divided by annual debt service. Measures ability to service debt from property income. Required by most lenders. | Minimum 1.25x; target 1.5x+ for comfortable debt coverage | High (for debt financing) |

For detailed operational benchmarks across 200+ operators, see our 2025 Global Coliving Report. For business model economics, see Coliving Business Models.

Over $5 billion in capital has flowed into coliving through these landmark deals. Understanding the investor landscape helps you identify the right capital partners.

| Company | Amount | Investors | Year |

|---|---|---|---|

| Colonies (France) | €1B | Ares Management | 2023–24 |

| Cohabs (Belgium) | $450M | Ivanhoé Cambridge, Belfius, Belgian sovereign wealth | 2023 |

| CapitaLand CLARA II | $600M | CapitaLand Ascott | 2024 |

| COLIV Fund (DTZ/Collective) | £650M | DTZ Investors + The Collective | 2019–24 |

| Medici Living (QUARTERS) | $1.44B | Corestate Capital, W5 Group | 2018–20 |

| Greystar (Spain portfolio) | ~€300M | Greystar (acquired from Bain Capital) | 2025 |

| CoLive (India) | $100M+ | Bain Capital + Sattva Group | 2024 |

| PadSplit (US) | $35.2M | Core Innovation Capital, Impact Engine, Citi, Mark Cuban | 2019–21 |

Key investor types: banks (27% of financing), PE/VC firms, family offices, and impact investors. The institutional entry is accelerating — €2.6B committed across Europe by 2025.

Follow the 10/20/30 rule: 10 slides, 20 minutes, 30pt minimum font. Lead with your most impressive metric. Capital efficiency beats growth speed in 2025.

Housing affordability crisis, loneliness epidemic, demographic shifts (remote work, single households). $7.8B market growing at 11%+ CAGR.

Tip: Use local market data. Show the gap between housing costs and income growth in your target city.

Your coliving concept — the physical space, community model, technology platform, and resident experience. Show the UCX journey.

Tip: Photos and floor plans > slides of text. Show what makes your space different from a shared apartment.

Revenue model (per-bed pricing, membership, services), cost structure, gross margins, path to NOI. Show per-property P&L.

Tip: Investors compare coliving to traditional residential. Show the 40–50% income premium and the NOI uplift.

Occupancy rates, RevPAB, resident retention, community engagement scores, NPS, waitlist demand. Quantify everything.

Tip: Lead with your most impressive metric. If 95% occupied with 60% referred, that's your opening slide.

TAM/SAM/SOM framework. Show coliving as % of total residential stock in your market. Reference the 87% YoY UK planning growth.

Tip: Be specific to your geography. A $7.8B global market is less compelling than '12,000 target residents in Berlin'.

Position vs traditional rental, co-living competitors, and Build-to-Rent. Show your defensible differentiation — community, design, location.

Tip: Don't claim 'no competition.' Show you understand the landscape and have a clear wedge.

Founder backgrounds in real estate, hospitality, tech, and community. Advisory board. Key hires planned with this round.

Tip: Post-Common bankruptcy, investors scrutinize team operational experience heavily. Real estate + operations background is essential.

3–5 year revenue, occupancy, NOI, and cash flow projections. Show per-property and portfolio-level economics.

Tip: Be conservative. Show unit-level profitability early, then portfolio growth. Capital efficiency > growth speed in 2025.

Amount raising, valuation (if priced), allocation: property acquisition/lease (60–70%), operations buildout (15–20%), tech & team (10–20%).

Tip: Show the capital bridge — how this round gets you to the next milestone (more properties, institutional-grade reporting, Series A readiness).

Our team has helped coliving operators raise capital and refine their investor presentations across 14+ countries.

These high-profile failures reshaped the coliving investment landscape. Understanding them is essential for any fundraising conversation — investors will ask about them.

Chapter 7 bankruptcy — June 2024

Once the largest North American coliving operator: 5,200 units across 12 cities. Raised $110M+ in venture capital. Assets: up to $10M vs liabilities: $50M+.

Key lesson: Aggressive expansion on master leases without proven unit economics. Rising interest rates and overhead costs collapsed margins. Capital efficiency > growth speed.

Bankruptcy — 2021

Raised $1.44B total funding. Despite massive capital, operational challenges and COVID-19 led to insolvency. Properties taken over by Outpost Club.

Key lesson: Massive fundraising doesn't equal sustainability. Unit-level profitability must precede scaling. Debt leverage amplifies both gains and losses.

Shutdown — 2019

Early coliving startup that relied on sublease agreements. Unable to scale profitably. Agreements taken over by Outpost Club.

Key lesson: Sublease-only models are fragile. Lack of property control creates existential risk when landlords can terminate leases.

The common thread: aggressive scaling without proven unit economics. In 2025, investors prize capital efficiency, sustainable growth, and demonstrable property-level profitability above growth speed.

Beyond traditional equity and debt, coliving operators can access crowdfunding, government grants, and impact financing — especially when positioned as affordable housing.

Platforms like Republic, Wefunder, and StartEngine allow coliving operators to raise from community investors. Investment crowdfunding reached $447M in H1 2025 (+60% YoY).

Best for: Best for early-stage operators building community investor networks and brand awareness.

Fractional ownership via blockchain — 22% of new developments now use blockchain-backed smart contracts for fund disbursement. Opens coliving investment to smaller investors.

Best for: Best for operators targeting tech-savvy investors and innovative capital structures.

ESG-linked loans with favorable terms. The Social Hub secured €145M from UniCredit with ESG conditions. Green crowdfunding grew 35% in 2024.

Best for: Best for operators with genuine sustainability credentials and social impact metrics.

The largest US federal housing subsidy — tax credits to developers of affordable housing. Coliving naturally qualifies when designed as affordable housing.

Best for: Best for US-based operators targeting below-market-rate housing with community model.

Federal HOME program (~$1B annually) and state housing trust funds provide grants and loans for affordable housing development.

Best for: Best for operators in markets with strong affordable housing policy frameworks.

Capital gains tax deferral for investment in designated zones. Many gentrifying neighborhoods (prime coliving locations) qualify as opportunity zones.

Best for: Best for investors seeking tax-advantaged coliving investment in transitional neighborhoods.

Our Global Coliving Report provides market trends, operational benchmarks, and financial metrics from 200+ operators.

It depends on your model. A master-lease operator can launch with $50K–200K (security deposits, furnishing, first/last month rent). Direct ownership requires $500K–5M+ depending on the market. Management agreements need minimal capital — just operational working capital. Most successful operators start with 1–2 properties to prove unit economics before raising external capital. The key is demonstrating positive unit economics at small scale before scaling.

The five metrics that matter most: occupancy rate (target 90%+, industry average 93–94%), RevPAB (Revenue Per Available Bed — the primary performance metric), NOI and NOI margin (coliving densification increases NOI 10–30% over traditional residential), CAC and LTV:CAC ratio (target 3:1+), and resident retention rate. For debt financing, DSCR (Debt Service Coverage Ratio) of 1.25x+ is typically required. Cap rates of 4–7% and IRR targets of 15–25% for value-add deals are standard institutional benchmarks.

For seed-stage coliving operators, SAFEs (Simple Agreements for Future Equity) dominate — they represent 64% of all seed deals in 2024. SAFEs are simpler, faster, and protect both parties. For growth-stage, priced equity rounds (Series A Preferred) provide clearer governance. For property-level investment, DSCR loans are popular because they focus on projected property income rather than personal earnings. Post-Common bankruptcy, investors favor operators who demonstrate capital efficiency and sustainable growth over aggressive expansion.

Coliving consistently outperforms traditional residential on a per-square-foot basis: 40–50% more rental income than traditional apartments, 44% more income per square foot, and 10–30% higher NOI through densification. In specific markets: Sydney coliving yields 4% vs 2.6% traditional; Hong Kong 3.4% vs 2.2%; India 10–13% vs 3% traditional. PadSplit hosts earn 33% more than Airbnb and 2.5x more than traditional long-term rental. However, coliving has higher operational complexity and turnover costs.

Post-2024, the market has shifted away from master leases for institutional fundraising. Common Living's bankruptcy ($110M+ raised, $50M+ liabilities) was driven by aggressive master-lease expansion. Institutional investors now prefer: direct ownership (highest returns, best control), management agreements (lowest risk, fastest scaling), or hybrid models (co-investment with real estate partners). Master leases work for early validation but are harder to raise institutional capital against. If using master leases, ensure performance-based rent structures and strong landlord relationships.

Nine essential sections: Problem & Market (housing crisis, $7.8B market), Solution & Product (your concept and UCX), Business Model & Unit Economics (per-bed pricing, P&L), Traction & Metrics (occupancy, RevPAB, retention), Market Opportunity (TAM/SAM specific to your geography), Competitive Landscape (positioning vs rentals and co-living peers), Team & Track Record (real estate + operations experience), Financial Projections (3–5 year NOI and cash flow), and The Ask (amount, valuation, use of funds). Follow the 10/20/30 rule: 10 slides, 20 minutes, 30pt minimum font. Lead with traction.

The global coliving market was valued at $7.82 billion in 2024 and is projected to reach $15.9 billion by 2025, growing at 11–13.5% CAGR. Asia-Pacific leads (48% market share), followed by Europe (22%) and North America (18%). There are 827 coliving startups globally, with 234 funded and 80 having raised Series A+. Institutional engagement is accelerating: 38% of European investors with €1T+ AUM are already invested in coliving; 51% plan to invest within 3 years. The UK alone saw an 87% increase in coliving planning applications in 2024.

Yes, when coliving is positioned as affordable housing. Key US programs: LOW INCOME HOUSING TAX CREDIT (LIHTC) — the largest federal housing subsidy via tax credits; HOME Investment Partnerships (~$1B annually for affordable housing); National Housing Trust Fund for extremely low-income housing; and Opportunity Zone incentives for capital gains deferral. State and local housing trust funds, city-specific affordable housing grants, and ESG-linked financing (like UniCredit's €145M to The Social Hub) are also available. The key is framing coliving as an affordable housing solution — which it genuinely is, offering 20–40% lower per-person costs than traditional housing.

Common Living, once the largest North American coliving operator (5,200 units, 12 cities), filed for Chapter 7 bankruptcy in June 2024 after raising $110M+ in venture capital. Assets: up to $10M; liabilities: $50M+. The primary causes: aggressive expansion on master leases without proven unit economics, rising interest rates compressing margins, and overhead costs that grew faster than revenue. The lesson for operators: prove unit-level profitability before scaling, prefer management agreements or ownership over pure master leases, and prioritize capital efficiency. Investors now heavily scrutinize burn rates and path to profitability.

Institutional investors (€1T+ AUM) look for: institutional-grade financial reporting, 1,000+ beds under management (or clear path to it), experienced management team with real estate operations background, demonstrable NOI track record, technology-enabled operations, and ESG/impact credentials. The entry points are dedicated coliving funds (DTZ's COLIV Fund, CapitaLand's CLARA II), real estate PE firms (Ares, Bain Capital, Greystar), and impact investors. Build relationships early — attend MIPIM, ULI conferences, and coliving industry events. Our advisory team can help with investor introductions.

PropTech venture capital totaled $16.7–19.4 billion globally in 2024. For coliving operators, a strong technology stack signals operational maturity to investors. Key tech components: property management software (resident lifecycle, billing), community management platform (engagement, events), revenue management (dynamic pricing, occupancy optimization), smart building systems (IoT, energy management), and data analytics (KPI dashboards, investor reporting). AI-powered automation is particularly attractive — $3.2B was invested in AI PropTech in 2024 alone. Investors prefer companies that deliver measurable automation ROI.

Yes. The global alternative finance market reached $260B in 2024. Four models apply to coliving: equity crowdfunding (investors get ownership stake), debt/P2P lending (revenue-share agreements), reward-based (perks like discounted stays), and real estate tokenization (fractional ownership via blockchain — 22% of new developments now use blockchain smart contracts). Equity crowdfunding platforms like Republic, Wefunder, and StartEngine can support coliving raises. However, institutional investors typically prefer traditional equity or debt structures. Crowdfunding works best for early-stage operators building community investor networks.

Deep dives into coliving financial models, investment structures, and industry trends.

If you came to this article directly, consider going through the series of articles it is a part of. Please find the link to the other articles in the...

June 11, 2025

If you came to this article directly, consider going through the series of articles it is a part of. Please find the link to the other articles in the...

June 10, 2025

If you came to this article directly, consider going through the series of articles it is a part of. Please find the link to the other articles in the...

June 9, 2025

If you came to this article directly, consider going through the series of articles it is a part of. Please find the link to the other articles in the...

June 8, 2025

If you came to this article directly, consider going through the series of articles it is a part of. Please find the link to the other articles in the...

June 7, 2025

If you came to this article directly, consider going through the series of articles it is a part of. Please find the link to the other articles in the...

June 6, 2025

If you came to this article directly, consider going through the series of articles it is a part of. Please find the link to the other articles in the...

June 5, 2025

If you came to this article directly, consider going through the series of articles it is a part of. Please find the link to the other articles in the...

June 4, 2025

If you came to this article directly, consider going through the series of articles it is a part of. Please find the link to the other articles in the...

June 3, 2025

If you came to this article directly, consider going through the series of articles it is a part of. Please find the link to the other articles in the...

June 2, 2025

If you came to this article directly, consider going through the series of articles it is a part of. Please find the link to the other articles in the...

June 1, 2025

Explore more in our Coliving Finances blog category.

BookMyColiving.com is a free platform for coliving operators to list their spaces, generate qualified leads, and grow profitably. No commissions, no listing fees — just direct connections with travelers and remote workers looking for their next coliving home.

From deal structuring to investor introductions — our advisory team has helped 60+ coliving operators raise capital, refine financial models, and connect with the right investors across 14+ countries.

Monthly masterminds, weekly updates, and networking with coliving operators worldwide.